Energy

Why stable power supply may remain elusive

• Over 60% of power plants unavailable for transmission in Q3 2025, says report

• Report exposes Discos culpability

• NERC may sanction erring entities

The state of electricity supply in the country has become a source of concern for residents. After enjoying a relative supply for some parts of last year, especially in the second quarter, drawing applause from consumers, the euphoria that greeted this has gradually becoming worrisome.

These concerns were more pronounced during the last yuletide, when several homes were left in the dark. The situation, electricity Distribution Companies (DisCos) often explain, results from national grid collapses, low power generation, gas supply shortages, or maintenance work by the Transmission Company of Nigeria (TCN). These issues, alongside infrastructure decay and vandalism, invariably leads to load shedding and intermittent supply.

Top officials of some Discos spoken to who pleaded for anonymity attributed power failures to a mix of upstream generation deficits, national grid instability and localised infrastructure challenges.

For a long time, there has been several horse-trading associated across the value chain over erratic power supply. For instance, it is common for DisCos often cite “system-wide disturbances” or “grid collapses” from the National Control Centre (NCC) as the reason for total outages across their franchise areas. Besides, many outages are blamed on “gas limitations” at thermal power plants and a general drop in power generation. This is because when generation drops, the energy allocated to DisCos decreases, forcing them to implement load shedding.

In situations like this, most hide under the guise of the feeder banding system. Under this framework, priority is given to “Band A” feeders, which are mandated to receive 20+ hours of supply thereby often leaving lower bands with significant outages when total available power is low.

Yet, is the technical faults and maintenance of equipment, equipment vandalism like destruction of transformers and theft of cables; planned maintenance, like upgrading or repairing transmission lines, are also factor readily given as excuses by service providers.

After enjoying relative stability in national grid in 2025, the facility experienced a first major collapse at the weekend caused by the simultaneous tripping of multiple 330kV transmission lines.

With this incident coming early in the year, stakeholders are worried that it may not be a good omen for the sector notwithstanding the several assurances by government. In 2024, 12 grid collapses were recorded; 12 in 2025 and one already recorded this year.

More worrisome is that the epileptic power supply has remained irrespective of the fiscal appropriation to the sector under the President Bola Tinubu administration.

A cursory look at these allocation indicate that in the last three years, there has been a consistent increase in fiscal allocation to the Ministry of Power aimed at resolving the underlying issues that have consistently impeded growth in the sector, including the consistent grid collapses each year.

A breakdown of the figures the three years showed that the power ministry got a cumulative allocation of N239.5 billion in 2023; N344.097 billion in 2024; N2.1 trillion in the 2025 budget, a clear indication of the priority placed on the sector by the current administration.

A further breakdown of the figures show that the power sector recovery programme received N810 billion from the budget; special intervention project got N269.74 billion, while the presidential power initiative (PPI) transmission project received N150 billion, all in an attempt to tackle the enormous challenges in the nation’s power sector from specific and targeted approach.

The Minister of Power, Adebayo Adelabu, assured that the ministry has set the agenda for Nigeria’s power sector in the year 2026, suggesting that the country has done enough to stabilise its grid in the previous year.

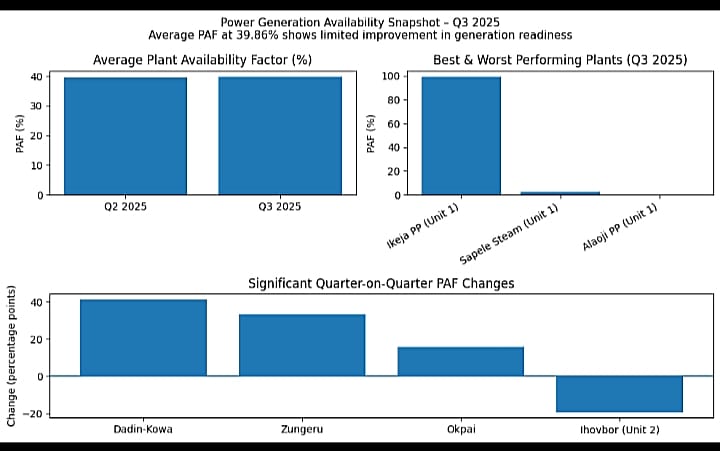

But these challenges appear unresolved despite huge budgetary allocations to the power sector. Giving more insight into what may be the cause of the deep-seated challenges confronting the country’s electricity supply is a recent report by the Nigerian Electricity Regulatory Commission (NERC) for the third quarter of 2025. The report, released recently, indicated that over 60 per cent of power plants installed generation capacity in the country remained unavailable for transmission to the national grid in the third quarter of 2025.

According to the NERC report, the average Plant Availability Factor (PAF) of all 28 grid-connected power plants stood at 39.86 per cent, meaning that 60.14 per cent of installed capacity could not be dispatched to the national grid at any point during the quarter. The figure represents only a 0.26 percentage-point increase from the 39.60 per cent recorded in Q2 2025, highlighting how limited progress has been in improving the operational readiness of generation assets.

“In 2025/Q3, the average plant availability factor for all grid-connected plants was 39.86 per cent, that is, at any point in time during the quarter, 60.14 per cent of the installed capacity across the 28 grid-connected power plants was not available for dispatch onto the grid,” the report read.

The PAF measures the ratio of a power plant’s declared available capacity to its manufacturer-rated installed capacity and is widely regarded by regulators as a key indicator of the health of the upstream segment of the Nigerian Electricity Supply Industry (NESI).

It further noted that while 11 power plants recorded availability above 50 per cent, Ikeja Power Plant (Unit 1) emerged as the best-performing asset, posting a PAF of 99.24 per cent during the quarter. At the lower end, Sapele Steam Plant (Unit 1) recorded a PAF of just 2.66 per cent, while Alaoji Power Plant (Unit 1) failed to dispatch any electricity at all throughout the quarter.

Significantly quarter-on-quarter improvements were recorded at Dadin-Kowa (+41.32pp), Zungeru (+33.29pp) and Okpai (+15.95pp), reflecting gains from improved hydrology and reduced outages.

However, availability declined sharply at Ihovbor (Unit 2), which fell by 19.21 percentage points to 78.16 per cent, down from 97.38 per cent in Q2. Other plants that recorded notable drops included Geregu (Unit 1), Ibom Power, and Geregu (Unit 2).

“Overall, 11 power plants had availability factors above 50 per cent, with Ikeja_1 power plant recording the highest availability factor at 99.24 per cent. On the other end of the spectrum, Sapele Steam_1 recorded a PAF of 2.66 per cent in 2025/Q3. Alaoji_1 power plant was not available to dispatch any energy onto the grid throughout the quarter.

“Significant increases in PAF were recorded in Dadin-Kowa_1 (+41.32pp), Zungeru_1 (+33.29pp), and Okpai_1 (+15.95pp) power plants across the two quarters. Conversely, the PAF of Ihovbor_2 decreased significantly by 19.21pp during the quarter (78.16 per cent in 2025/Q3 compared to 97.38 per cent in 2025/Q2). Reductions in PAF were also recorded in Geregu_1 (- 12.79pp), Ibom power_1 (-10.34pp), and Geregu_2 (-8.41pp) power plants,” the NERC report said.

The commission attributed the fluctuations in plant availability to mechanical outages, feedstock constraints, hydrological conditions and operational limitations, factors that have continued to undermine Nigeria’s generation capacity for over a decade.

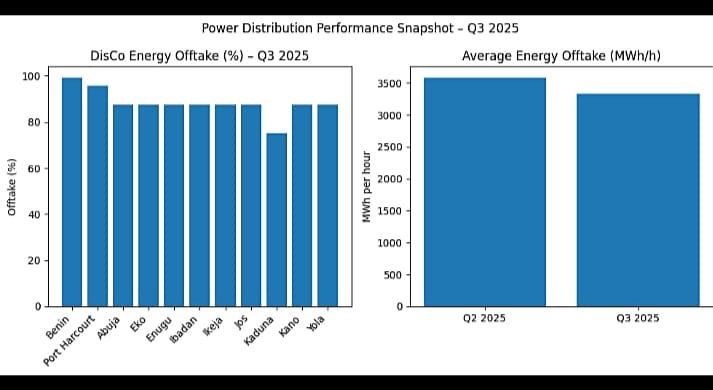

Beyond generation challenges, the report also highlighted weak energy offtake by electricity Discos, raising concerns over revenue recovery and market discipline. Under the Partial Activation of Contract regime, which came into force in July 2022, DisCos are required to off-take and pay for their Partially Contracted Capacity on a take-or-pay basis, even if they fail to utilise the power.

In Q3 2025, average energy offtake by DisCos fell to 3,328.33 megawatt-hours per hour, representing a 7.10 per cent decline from 3,582.62MWh/h recorded in the preceding quarter.

This decline occurred despite the fact that available contracted capacity dropped by only 2.43 per cent, suggesting that generation and transmission availability were sufficient to sustain previous offtake levels.

Overall, cumulative DisCo energy offtake performance during the quarter stood at 87.39 per cent, down from 91.78 per cent in Q2, a 4.39 percentage-point decline.

“All DisCos except Jos recorded a decline in their energy offtake performance during the quarter,” the report noted.

The commission attributed the reduced offtake to a combination of infrastructure weaknesses, seasonal demand changes and commercial considerations.

It noted that frequent network outages during the rainy season, driven by fragile distribution infrastructure, limited the ability of DisCos to evacuate power to customers.

In addition, cooler weather conditions reduced domestic electricity demand, while some DisCos deliberately constrained supply to loss-prone feeders to minimise financial exposure.

Under the Performance Monitoring Framework Orders issued in July 2024, DisCos are required to off-take at least 95 per cent of their available PCC or face regulatory sanctions.

However, in Q3 2025, only Benin and Port Harcourt DisCos met the threshold, with offtake levels of 99.20 per cent and 95.65 per cent, respectively.

The remaining nine DisCos, Abuja, Eko, Enugu, Ibadan, Ikeja, Jos, Kaduna, Kano and Yola, fell short, with Kaduna DisCo recording the lowest performance at 75.23 per cent.

“The Commission has commenced the implementation of appropriate sanctions against defaulting DisCos,” the report stated.

The figures reflect the persistent mismatch between installed capacity, available generation, and effective electricity delivery, a challenge that continues to frustrate households and businesses.

Despite Nigeria’s installed generation capacity exceeding 13,000 megawatts, average operational availability and weak offtake mean that actual electricity delivered to consumers remains far below demand, reinforcing dependence on self-generation and driving up energy costs.

• It’s a mixed bag for Nigeria, says Dr. Muda Yusuf

Oil prices fell sharply yesterday following a peace deal secured between the U.S and Iran to end the war that began on February 28 and also an agreement to reopen the Strait of Hormuz more than 100 days after its closure.

By yesterday, Brent crude had dropped by about 4.53 per cent to trade at $83.37 per barrel, while West Texas Intermediate (WTI) had fallen 4.69 per cent to $80.90 per barrel. Oil prices, which peaked in mid-May, have been slowly but surely trending downward in recent weeks on rumors of a deal, even after multiple escalatory strikes.

An economist and policy analyst, Dr. Muda Yusuf, described the development as a mixed bag for Nigeria. According to him, while the price drop will naturally translate to a reduction in the pump prices of petrol, diesel, Jet A1 and gas, on the flip side, it portends a drop in revenue for the federal government.

“With the peace deal, crude oil prices will plummet and naturally this should cascade into the local oil market. So I expect that petrol prices should revert to what it used to be before the war. However, this will not be immediate because many of these distributors are carrying old stock, which they bought at a higher price before today (yesterday). Remember that the Middle East is a major producer and supplier to the market; Qatar has left OPEC, so they will be free now to flood the market, meaning we are likely to see an even more drastic reduction in price.

“However, the price reduction is likely to be gradual. But within the next four weeks or so, the situation should normalise and prices should come down to what normally it used to be. It should come to pre-war situation. If oil price comes to around $65 or so, then it should come to close to N800 or N900 per litre,” he said.

According to Yusuf, who is also the Chief Executive Officer, Center for the Promotion of Private Enterprise (CPPE), there is also a flip side to the price reduction for Nigeria.

“The flip side for Nigeria’s revenue is going to be negative because for all producing countries that were not caught up in this Middle East or Strait of Hormuz problem, who have been benefiting from the windfall, of course this will mean that the windfall will disappear. And earnings from crude oil will also affect revenue negatively.

“So we are likely to see a reduction in our oil revenue arising from this deal or the likely drop in crude oil price. It’s a no-brainer. The revenue will drop and of course it means that there are some benefits and some demerits,” Yusuf submitted.

The peace agreement, which will be formally signed on Friday in Switzerland, got further boost when President Donald Trump declared that a deal with Iran was complete, and writing on social media that “oil will flow” through the Strait of Hormuz once the deal is signed on Friday.

The peace deal remains very significant for the global oil market as tension around the commodity is expected to ease up. Iran, for instance, will be able to resume crude exports during the 60-day ceasefire period, meaning a suspension of sanctions on Iranian oil, while broader nuclear negotiations continue.

Stakeholders argued that while the agreement represents the most serious diplomatic breakthrough since the war began, they are however concerned that oil markets will remain on edge until the Strait of Hormuz is cleared of mines, the deal is signed, and normal shipping flows resume.

Axxela Limited has announced the appointment of new non-executive Board members to deepen strategic oversight and strengthen corporate governance in support of the company’s next phase of exponential growth.

The newly appointed Board members are Nzan Ogbe (Chairman of the Board), Eric Idiahi, Dolu Olugbenjo, Olufemi Okin, Moshood Olajide, Kaat Van Hecke and Jeremy Bending. Their combined experience in business leadership, financial management, and infrastructure development will strengthen the company’s post-divestment governance framework and guide the company as it expands its gas infrastructure footprint and delivers sustainable energy solutions across industries and markets.

Nzan Ogbe, Chairman of the Board, is the founder and first CEO of Levene Energies and the chairman of LPV Energies. He is a serial entrepreneur with over 30 years of experience building businesses across sectors, including commercial trading, energy, real estate, and telecoms. His leadership and commitment to sustainability have established him as one of Africa’s most resourceful business leaders.

Eric Idiahi is a seasoned entrepreneur and strategic investor with over 20 years of experience building and backing businesses that are shaping Africa’s future. He co-founded Evercorp Industries and previously served as a partner at Verod Capital Management. He has raised more than $1 billion for businesses across key sectors of the African economy.

Dolu Olugbenjo is an Executive Director at Stanbic IBTC Asset Management and serves as Chief Investment Officer of the Stanbic IBTC Infrastructure Fund. He has over 20 years of experience, including leading debt advisory transactions for a wide range of clients.

Moshood Olajide is an experienced oil and gas industry operator with an extensive track record in operational excellence, business growth, and strategic transformation. He holds a Bachelor of Laws degree from Obafemi Awolowo University and a Master of Law degree from Columbia University in New York. He is a fellow of the Association of Chartered Certified Accountants and licensed to practice law in Nigeria and New York. He takes over from Timothy Ononiwu as the new Group Chief Executive Officer.

Kaat Van Hecke has over two decades of relevant professional experience spanning several jurisdictions, including Nigeria, Austria, the Netherlands, Russia, and Kazakhstan. She serves as an Independent Non-Executive Director in Serica Energy PLC, London/Aberdeen, and in Trinity Exploration and Production PLC, London/Trinidad and Tobago.

Jeremy Bending has wide experience of unbundling and market liberalization in the UK energy industry. He is also experienced in international M&A activities and disposals. He is a Chartered Engineer who has been closely involved in implementing and maintaining safety and engineering management systems.

Olufemi Okin is a seasoned financial services executive with over a decade of progressive experience, spanning trusteeship, capital markets, corporate governance and legal advisory services. He is recognised for driving sustainable profitability, securing high-value corporate and public trust mandates, and fostering strong relationships across key stakeholders.

Speaking on the Board appointments, the Chairman, Nzan Ogbe, said, “It is a privilege to assume the role of Chairman and to work alongside my fellow directors and the management team to provide strong governance, strategic oversight, and guidance as the company continues its growth journey.”

The new board members bring a wealth of experience across oil & gas, banking, consulting, asset management, and private equity, and are well-positioned to strengthen oversight and drive sustainable growth.

As Axxela continues to expand its infrastructure investments and deepen its role in advancing cleaner, more reliable energy solutions, the expertise and perspective of the new board members will be key to shaping the company’s strategic direction.

The international oil market tumbled at the weekend as U.S.-Iran peace negotiations gain momentum. As at the time of going to press last night, words were still being awaited of the signing of a peace deal between the U.S and Iran to end the war- a position the U.S President, Donald Trump, had maintained would happen and lead to the full reopening of the Strait of Hormuz.

But experts caution that a return to pre-war oil price levels remains a distant prospect. The reopening of the Strait of Hormuz, experts say, does not, in itself, signal an immediate normalisation of energy supplies.

Still, forecasts for oil are split, with Goldman Sachs lowering its 2027 Brent crude outlook to $80 per barrel, while ING warns prices could spike to $120–$130 if supply disruptions persist.

Biggo.com news, quoting the Seoul Economic Daily’s energy series “Petro-Electro” and Reuters, noted that the market’s primary focus is now on whether the so-called “Islamabad Declaration”—a memorandum of understanding (MOU) to end hostilities between the U.S. and Iran—will be signed.

Reuters reported that the two nations have agreed to reopen the Strait of Hormuz within 30 days in exchange for releasing billions of dollars in frozen Iranian assets and waiving sanctions on Iranian crude exports. Negotiations over Iran’s nuclear programme are also slated to proceed for 60 days following the cessation of hostilities.

Based on these, Brent crude futures fell $3.05, or 3.37 per cent to settle at $87.33 per barrel, marking their lowest level since early March. West Texas Intermediate (WTI) also dropped $2.83 or 3.23 per cent to $84.88 per barrel, its weakest since April 17.

However, reopening the strait does not equate to a full restoration of Middle Eastern energy flows. A severe bottleneck is inevitable as hundreds of vessels currently stranded in the Persian Gulf attempt to transit the narrow waterway simultaneously.

Javier Blas, an energy columnist for Bloomberg, noted: “We will see the simultaneous effort to evacuate trapped tankers while new vessels attempt to enter. There is no precedent for this, and no playbook exists.”

The recovery on the production side is also proving sluggish. Kuwait Petroleum Corporation estimates it will take six to eight weeks to restore roughly 70% of crude output after the strait reopens, with an additional month needed to bring the remaining 30% back online. As supply recovers only gradually, the extent of any oil price decline will be inherently capped.

A sharp drawdown in global petroleum inventories is another factor underpinning prices. According to the International Energy Agency (IEA), global oil stockpiles fell by 250 million barrels between February—when the conflict began—and May. Once peace is restored, efforts by governments and refiners to replenish strategic and commercial reserves are expected to generate additional demand, further limiting downside for crude.

Conversely, significant downward pressures on oil prices remain formidable. Just before the war, the dominant concern in global crude markets was oversupply. With non-OPEC producers such as the United States, Brazil, and Canada already poised to increase output, the United Arab Emirates’ (UAE) withdrawal from OPEC has amplified the potential for a supply surge. The UAE has long chafed under production quotas, and any unilateral move to boost output could intensify the glut.

On the demand side, China’s slowing oil consumption is particularly pronounced. In May, China’s average daily crude imports fell to 7.8 million barrels, down more than 3 million barrels from the roughly 11 million barrels per day maintained in recent years. The structural shift in energy consumption—driven by the expansion of electric vehicles and increased use of petrochemical feedstocks—is cited as the root cause.

Major institutions are also diverging in their oil price outlooks. Goldman Sachs has lowered its 2027 average Brent crude forecast to $80 per barrel, reflecting rising supply and weakening demand. OPEC, meanwhile, cut its 2026 global oil demand growth estimate from 1.17 million barrels per day to 970,000 barrels, but left the door open to a demand recovery by projecting an increase of 1.73 million barrels per day in 2027. ING analysts warned that “if Middle Eastern crude supply is not restored by the end of July, inventory levels and seasonal demand increases could send oil prices soaring to $120–$130 per barrel.”

Saadé, CEO of French shipping giant CMA CGM, told the French parliament that “even if a peaceful solution is reached in the coming weeks, there is no guarantee that another crisis will not erupt,” underscoring the persistence of geopolitical uncertainty. Indeed, Iran has indicated that terms could change before the MOU is signed and has firmly stated that its missile program will be excluded from negotiations.

Ultimately, even if peace materializes, international oil prices appear set to navigate a complex path toward a new equilibrium—one shaped by the interplay of shipping bottlenecks, delayed production restarts, lingering Middle Eastern tensions, and shifting global demand patterns.

….Culled from Biggo.com

-

Art & Life9 years ago

Art & Life9 years agoThese ’90s fashion trends are making a comeback in 2017

-

Business9 years ago

The 9 worst mistakes you can ever make at work

-

Entertainment9 years ago

The final 6 ‘Game of Thrones’ episodes might feel like a full season

-

Art & Life9 years ago

According to Dior Couture, this taboo fashion accessory is back

-

Entertainment9 years ago

The old and New Edition cast comes together to perform

-

Entertainment9 years ago

Mod turns ‘Counter-Strike’ into a ‘Tekken’ clone with fighting chickens

-

Sports9 years ago

Phillies’ Aaron Altherr makes mind-boggling barehanded play

-

Entertainment9 years ago

Disney’s live-action Aladdin finally finds its stars