Economy

Dangote signs $600m AFC loan facility to support fertiliser expansion

• Targets over $4b annual forex earnings

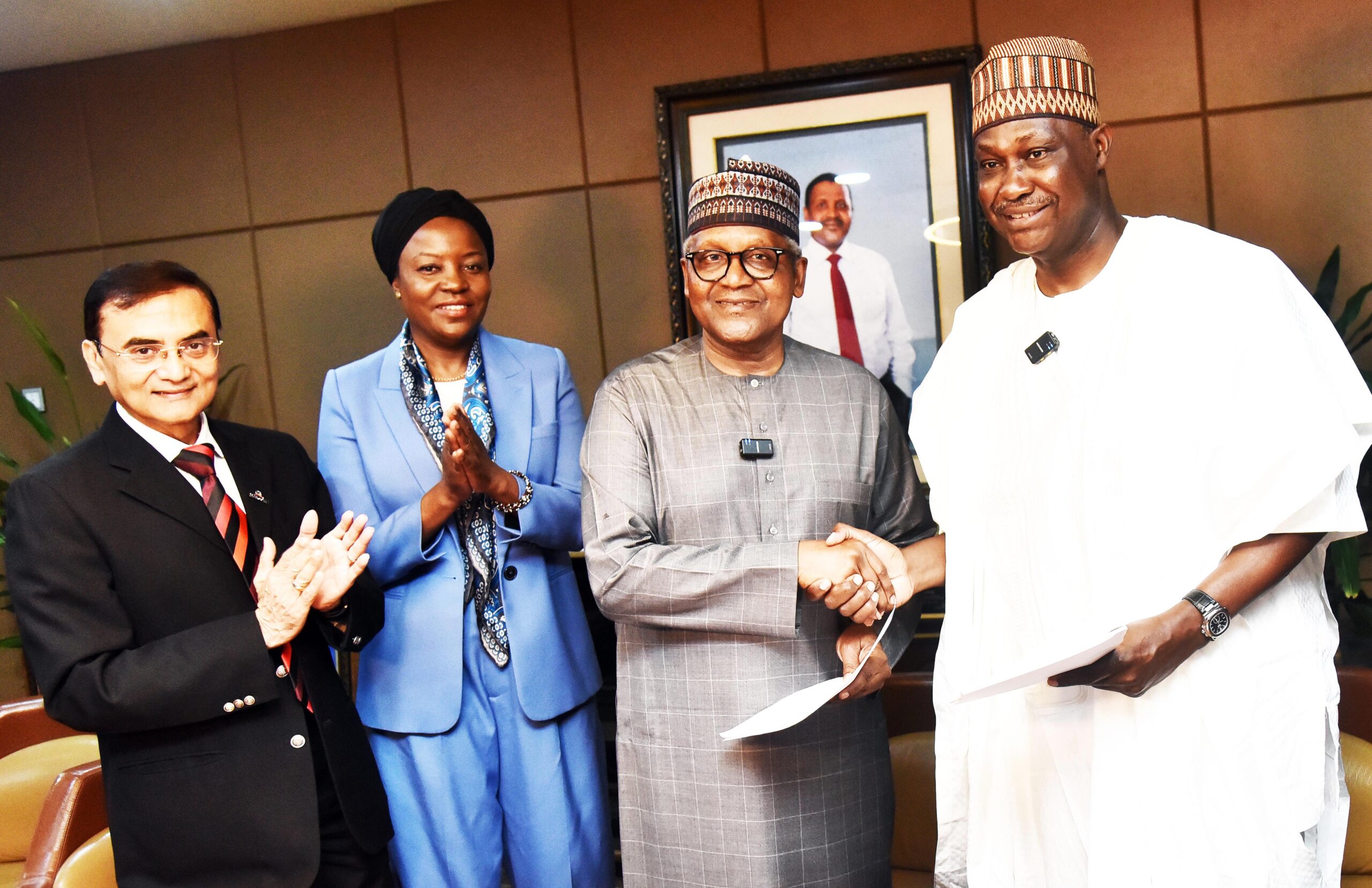

The Dangote Group has reinforced its long-standing partnership with the Africa Finance Corporation (AFC) through the signing of a $600 million loan facility to support the expansion of its fertiliser production capacity, an important milestone in advancing food security across Nigeria and the African continent.

The financing, extended to GreenView Fertilizer Corporation (Greenview), the Dangote Fertiliser Holding Company, will partly fund the expansion of urea production capacity in Nigeria as well as the development of a new fertiliser plant in Ethiopia.

This investment forms a key component of the Dangote Group’s broader $7 billion fertiliser expansion programme. The initiative is expected to increase production capacity in Nigeria from three million metric tonnes per annum (MTPA) to nine MTPA, while also supporting the establishment of a new three MTPA urea plant in Ethiopia.

Upon completion, the programme is expected to significantly boost Africa’s fertiliser output, strengthen regional food security, enhance agricultural productivity and reduce dependence on imports.

The facility underscores AFC’s strong confidence in Dangote Group’s vision to drive industrial growth and agricultural transformation through large-scale infrastructure investments. The funds will primarily support the ongoing expansion of the Dangote Fertiliser Plant at Ibeju-Lekki, Lagos, one of the largest granulated urea fertiliser complexes in the world.

The expansion is expected to substantially scale up production, improve supply chain efficiency, and ensure consistent availability of high-quality fertilisers to farmers across the continent. It will also contribute to price stability, reduce import dependency, and enhance crop yields, strengthening Africa’s overall food security framework.

Speaking on the development, President of Dangote Group, Aliko Dangote, said the expansion would generate significant foreign exchange earnings for the country.

“This investment positions us to deliver over $4 billion annually in fertiliser exports within the next three years. It represents a major contribution to Nigeria’s foreign exchange earnings and underscores our commitment to national economic growth. Our growth vision is not in isolation, we are building alongside strategic African partners like AFC and other institutions committed to the continent’s progress,” he explained.

President and CEO of AFC, Samaila Zubairu, highlighted the strategic importance of the deal.

“This transaction reflects AFC’s capital recycling model in action. Following the successful repayment of our earlier investment in Dangote Industries Limited, we are reinvesting and doubling that capital into Dangote Group’s next growth phase.

“By supporting the expansion of Dangote Fertilizer, AFC is backing a proven African industrial leader whose investments will strengthen food security, reduce import dependence, and create long-term economic value across the continent.”

This development builds on AFC’s strong track record of successful investments and exits across Africa, including projects in renewable energy, port infrastructure, digital connectivity, and industrial platforms.

The Dangote Fertiliser Plant currently plays a critical role in meeting domestic demand while exporting to international markets, thereby generating valuable foreign exchange for the country. With this new phase of expansion, the company is poised to consolidate its leadership position in the global fertiliser market while advancing Africa’s agricultural and economic resilience.

Nigeria’s Value Added Tax (VAT) collections rose to N2.42 trillion in the first quarter of this year, National Bureau of Statistics (NBS) data have shown.

The figure represents 17.06 per cent increase from the N2.07 trillion generated in the corresponding period of 2025.

The strong VAT performance recorded in the first quarter of 2026 reflects sustained economic activity across key sectors such as manufacturing, telecommunications, and mining.

The increase in VAT collections suggests that Nigeria’s non-oil revenue base continues to expand, providing additional resources for government spending and fiscal management.

The NBS also reported that VAT revenue grew by 9.98 per cent on a quarter-on-quarter basis from N2.20 trillion recorded in the fourth quarter of 2025, reflecting improved tax collections across key sectors of the economy.

Of the total VAT generated during the quarter, local payments accounted for N1.11 trillion, foreign VAT payments contributed N830.47 billion, while import VAT stood at N477.55 billion.

According to the NBS, several sectors recorded significant growth in their Value Added Tax (VAT) contributions during the first quarter of 2026, reflecting varying levels of economic activity across the country.

On a quarter-on-quarter basis, the strongest growth was recorded in activities of households as employers and undifferentiated goods-and-services-producing activities for own use, which surged by 74.36 per cent.

This was followed by the arts, entertainment and recreation sector, which expanded by 20.91 per cent, while the manufacturing sector posted a robust 12.82 per cent increase in VAT contributions.

Sectoral performance shows that education sector recorded the sharpest drop, with VAT contributions falling by 31.96 per cent. This was closely followed by public administration and defence, including compulsory social security, which declined by 31.38 per cent, while activities of extraterritorial organisations and bodies decreased by 29.89 per cent.

In terms of overall contribution to VAT revenue, the manufacturing sector maintained its position as the largest contributor, accounting for 29.75% of total collections in the first quarter.

The information and communication sector followed with 20.61%, underscoring the growing importance of digital and telecommunications services to the economy. Mining and quarrying ranked third, contributing 12.32 per cent of total VAT revenue.

At the lower end of the spectrum, activities of households as employers and undifferentiated goods-and-services-producing activities for own use accounted for just 0.01 per cent of total VAT collections.

Activities of extraterritorial organisations and bodies contributed 0.02 per cent, while water supply, sewerage, waste management and remediation activities made up 0.06 per cent.

The figures highlight the continued dominance of manufacturing, telecommunications, and extractive industries in Nigeria’s VAT revenue profile, while also reflecting the uneven pace of growth across different sectors of the economy.

The NBS added that overall VAT collections in Q1 2026 increased by 17.06 per cent compared with the same period of 2025.

VAT has emerged as one of Nigeria’s most important sources of non-oil revenue as the government intensifies efforts to diversify its income base and reduce dependence on crude oil earnings.

Nigeria’s positive assessment of her economic reforms by the International Monetary Fund (IMF) as contained in its Article IV Consultation Report, has drawn applause from economic expert and Chief executive Officer, Center for the Promotion of Private Enterprise (CPPE), Dr. Muda Yusuf.

He noted that the IMF’s acknowledgement of the progress made in restoring macroeconomic stability is broadly consistent with the position consistently advanced by CPPE and many stakeholders within the Nigerian private sector.

According to him, the reforms have helped to stabilise the foreign exchange market, improve external sector balances, strengthen investor confidence and restore a measure of policy credibility. Besides, Yusuf said the moderation in exchange rate volatility, the improvement in foreign reserves, the recovery in capital inflows and the stronger performance of many quoted companies underscore the positive outcomes of the stabilisation measures undertaken over the past three years.

“These gains are significant. After years of macroeconomic distortions, the economy is gradually moving from a regime of instability to one of greater predictability. This is an important foundation for investment, productivity and sustainable growth,” Dr. Yusuf said.

The CPPE, he said, equally agrees with the IMF’s concern about the persistence of poverty and food insecurity despite the progress made on macroeconomic stabilisation. This is because economic reforms are ultimately judged not only by their impact on macroeconomic indicators but by their ability to improve the welfare of citizens. He argued that while exchange rate stability, reserve accumulation and fiscal consolidation are important, however, he said, the true test of reform is whether they translate into lower food prices, better jobs, improved incomes and enhanced living standards.

He therefore proffered that the next phase of economic management should focus on converting macroeconomic gains into welfare gains, noting that the challenge before policymakers is no longer merely one of economic stabilisation but increasingly one of inclusive prosperity.

Yusuf warned of a situation that may lead to a risk of extreme monetary orthodoxy. According to him, while the IMF’s support for monetary tightening reflects conventional stabilisation thinking, he nonetheless expressed worries about the IMF’s continued emphasis on high interest rates without sufficient consideration of the adverse consequences for investment, enterprise growth, job creation and sovereign debt service pressures.

“The current monetary policy stance has delivered some benefits in terms of inflation moderation and exchange rate stability. However, every policy instrument has a point of diminishing returns. Beyond that point, the costs may begin to outweigh the benefits.

“The cost of credit in Nigeria has reached levels that are becoming increasingly prohibitive for productive investment. Lending rates remain among the highest in the world, making it difficult for businesses to expand, invest or create jobs.

“High yields on government securities have also intensified the crowding-out effect in the financial system. Banks and investors are increasingly channeling resources into treasury bills and government bonds rather than financing productive sectors of the economy. As a consequence, capital is gravitating towards financial assets rather than productive assets.

“An economy cannot achieve sustainable development when financial capital earns higher returns from government financial instruments than from supporting enterprise, innovation and industrialization,” Dr. Yusuf argued.

He also flayed the IMF for not sufficiently appreciating the developmental role of targeted financing interventions in an economy like Nigeria. He explained that development finance is not merely a policy choice, but an economic necessity. He warned that leaving such entirely to market forces, critical sectors such as agriculture, manufacturing, housing and infrastructure would remain chronically underfunded, thereby constraining productivity, job creation, industrialisation and long-term economic growth.

“Nigeria’s economic structure differs fundamentally from those of advanced economies. Strategic sectors such as agriculture, manufacturing, housing and infrastructure require long-term, patient capital which conventional market-based financing channels are often unable or unwilling to provide efficiently.

“In an economy where commercial lending is largely short-term, costly and risk-averse, development finance remains indispensable for unlocking productivity, supporting investment, expanding output and driving inclusive growth. A purely market-driven financing model cannot adequately address Nigeria’s structural financing gaps.

“Agriculture, for instance, cannot sustainably absorb commercial credit priced at prevailing market rates. Infrastructure projects often require financing tenors extending beyond what conventional banking structures can support.

“Development finance, therefore, should not be perceived as a distortion of the financial market; it is often a necessary response to market failure. Economic transformation has historically been supported by development finance institutions across both developed and emerging economies,” Dr. Yusuf warned.

Vice President Kashim Shettima and Lagos State Governor Babajide Sanwo-Olu has projected Lagos as Africa’s foremost investment destination, describing the state as the continent’s gateway to global wealth, trade and economic opportunities.

They spoke at the opening ceremony of Invest Lagos 3.0 held at Eko Hotels and Suites, Victoria Island, where policymakers, investors, development finance institutions and business leaders gathered to explore investment opportunities across key sectors of the economy.

Speaking on the theme: “Lagos: The Business Gateway to Africa, Powering Africa’s Next Era of Trade, Talent and Global Economic Leadership,” Shettima said Lagos was increasingly emerging as Africa’s gateway to global wealth and a strategic hub for international investors seeking access to the continent’s expanding markets.

According to him, Nigeria possesses the demographic strength, entrepreneurial talent and economic potential to rank among the world’s largest economies by 2050, provided the country continues to invest in innovation, infrastructure and effective leadership.

He noted that Lagos had sustained its position as Africa’s commercial nerve centre through deliberate policies, strong institutions and a business-friendly environment that continues to attract multinational corporations and foreign investments.

The Vice President also reaffirmed the Federal Government’s commitment to collaborating with states and the private sector to improve infrastructure, expand trade opportunities and strengthen the ease of doing business across the country.

In his keynote address, Governor Sanwo-Olu said Lagos had evolved significantly since the inaugural edition of the summit in 2024 and was strategically positioned to leverage opportunities presented by the African Continental Free Trade Area (AfCFTA).

He noted that with a population exceeding 23 million and a Gross Domestic Product (GDP) estimated at about $259 billion measured by purchasing power parity, Lagos remains the largest sub-national economy within the AfCFTA bloc.

”We are announcing to the world that if you want to reach Africa and benefit from its boundless market and economic potential, Lagos offers the most viable and appealing route,” the governor said.

Sanwo-Olu highlighted Lagos’ economic credentials, noting that the state handles about 70 per cent of Nigeria’s sea freight activities, hosts the country’s leading financial institutions and boasts one of Africa’s most vibrant startup ecosystems.

The governor outlined major infrastructure projects undertaken by his administration, including the Blue and Red Rail Lines, the operationalisation of the Lekki Deep Sea Port, the ongoing construction of the Fourth Mainland Bridge and plans for the Lekki-Epe International Airport.

He added that investments in agriculture, technology and logistics were transforming Lagos into a regional hub for food security and digital innovation.

Sanwo-Olu pointed to the emergence of globally recognised technology firms such as Flutterwave, Moniepoint, Andela and Interswitch as evidence of Lagos’ growing influence in Africa’s digital economy.

He also disclosed that the Lagos International Financial Centre (LIFC) project was progressing steadily and would serve as a major financial gateway connecting Africa to global capital markets.

The governor further revealed that Lagos had secured hosting rights for the Creative Africa Nexus (CANEX) 2026 and the Intra-African Trade Fair (IATF) 2027, describing both developments as evidence of growing international confidence in the state.

According to him, the summit’s deal rooms were deliberately designed to facilitate investment decisions and mobilise financing for critical projects.

”The singular goal is to spotlight and mobilise financing for the most consequential investment decisions across the public and private sectors that Nigeria has ever seen,” he said.

Sanwo-Olu added that the success of the summit would be measured not by attendance figures or speeches, but by investments capable of creating jobs and transforming lives.

Minister of Finance and Coordinating Minister of the Economy, Taiwo Oyedele, said ongoing fiscal and tax reforms were improving Nigeria’s investment climate, boosting investor confidence and creating new opportunities for economic growth across states.

Also speaking, Commonwealth Secretary-General Shirley Botchwey called for stronger regional cooperation through improved power supply, efficient logistics systems and enhanced security across Africa.

She urged African leaders to harness innovation and human capital as drivers of job creation and sustainable development.

Delivering the welcome address, Lagos State Commissioner for Commerce, Cooperatives, Trade and Investment, Folashade Ambrose-Medebem, described the summit as a strong vote of confidence in Lagos and its economic potential.

She said delegates, investors, business leaders and development partners from Nigeria, Africa, the Commonwealth and other parts of the world had gathered to explore opportunities in Africa’s largest commercial city.

According to her, Lagos remains Nigeria’s economic powerhouse and one of the world’s fastest-growing megacities, accounting for a significant share of national GDP while attracting the highest volume of domestic and foreign investments.

”Lagos is open for business, open for partnerships and open for investments. The opportunities are here, the market is here, the talent is here and the leadership is here,” she said.

Chairman of the Commonwealth Enterprise and Investment Council (CWEIC), Lord Marland, described Nigeria as a country with immense entrepreneurial potential and a critical player in Africa’s economic future.

He commended ongoing economic reforms and expressed optimism about Nigeria’s investment climate, noting that Lagos was well positioned to attract greater investment flows from across the Commonwealth and beyond.

A major highlight of the summit was the Governors’ Investment Showcase, where governors from Lagos, Abia, Imo, Nasarawa and Plateau states presented investment opportunities in key sectors of their economies.

The two-day summit was convened by the Lagos State Government in partnership with the Commonwealth Enterprise and Investment Council (CWEIC) to deepen investment partnerships and position Lagos as the preferred gateway to Africa’s next phase of economic growth.

-

Art & Life9 years ago

Art & Life9 years agoThese ’90s fashion trends are making a comeback in 2017

-

Business9 years ago

The 9 worst mistakes you can ever make at work

-

Entertainment9 years ago

The final 6 ‘Game of Thrones’ episodes might feel like a full season

-

Art & Life9 years ago

According to Dior Couture, this taboo fashion accessory is back

-

Entertainment9 years ago

The old and New Edition cast comes together to perform

-

Entertainment9 years ago

Mod turns ‘Counter-Strike’ into a ‘Tekken’ clone with fighting chickens

-

Sports9 years ago

Phillies’ Aaron Altherr makes mind-boggling barehanded play

-

Entertainment9 years ago

Disney’s live-action Aladdin finally finds its stars